Build Wealth

When it comes to your goals, we will work with you to establish the strongest foundations for building your financial future.

Protect Wealth

Ensuring you can manage and maintain your life, and your family’s life, is a big part of what we do. Whether it’s protecting yourself, your income, or your business, we’ll look at what works best for you.

Enjoy Wealth

Whether it’s planning for retirement or managing your time through retirement, our team has the expertise and understanding to work with you and your family.

FAQs

Financial planners may charge:

- Flat fees (eg. for a Statement of Advice)

- Hourly rates

- Ongoing service fees (combination of flat fees and percentage-based fees)

- Asset-based fees (a percentage of your portfolio)

At Parrish Financial, we offer transparent, upfront pricing with no hidden commissions.

If your finances are simple and you’re confident with budgeting and investing, DIY may work. But for major life events, complex portfolios, or long-term planning, a financial planner can provide tailored strategies, tax efficiency, and peace of mind.

Yes. A financial planner helps you make informed decisions, avoid costly mistakes, and optimise your finances for long-term success. Whether it’s managing investments, planning for retirement, or protecting your wealth, professional advice often delivers value far beyond the cost.

Some fees are tax deductible—particularly those related to managing income-producing investments or tax affairs. Initial advice fees are generally not deductible, but ongoing advice may be, depending on the nature of the service.

Key times include:

- Starting your career or family

- Buying property or receiving an inheritance

- Approaching retirement

- Navigating aged care or estate planning

- The earlier you start, the more value you can gain.

Our process follows a structured six-step model:

1. Discovery Meeting – Understand your goals and values

2. Data Collection – Review your financial position

3. Strategy Development – Tailored recommendations

4. Statement of Advice – Formal written plan

5. Implementation – Putting the plan into action

6. Ongoing Annual Review – Adjusting as your life evolves

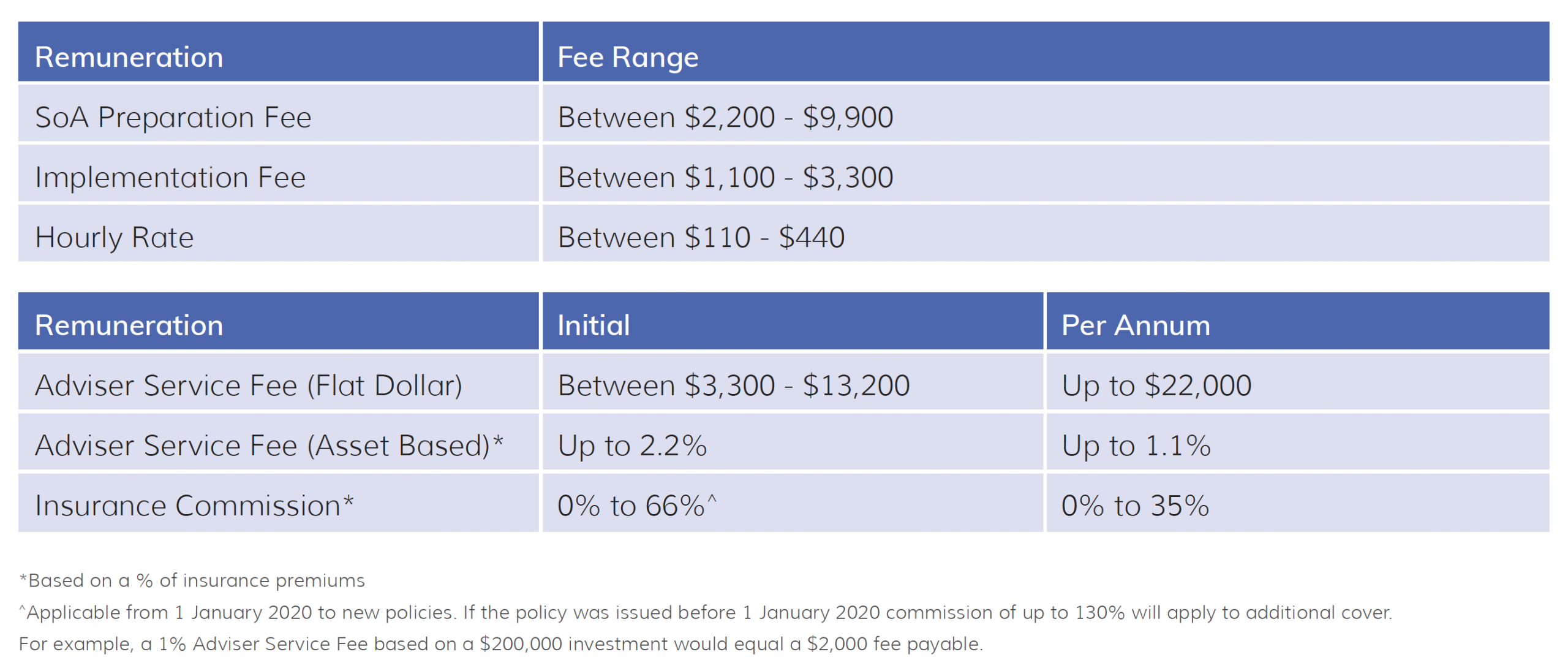

The cost of providing financial advice or service to you will depend on the nature and complexity of the advice, financial product and/or service provided. Your Adviser or the financial planning business may be remunerated by:

- Advice and service fees paid by you

- Commissions paid by insurance providers

The following table summarises the types of fees or commissions that are applicable to the services that we provide. Before providing you with advice, your Adviser will agree with you the fees that apply. All amounts are inclusive of Goods and Services Tax (GST).

We focus on:

- Wealth creation and protection

- Superannuation strategies

- Insurance

- Estate planning

- Retirement planning

- Aged care financial advice

Yes. Your initial meeting is obligation-free. It’s an opportunity to explore your goals and see how we can help.

Absolutely. We help clients optimise their superannuation and navigate aged care options, including funding strategies and Centrelink entitlements.

We recommend annual reviews, or more frequently if your circumstances change—such as a new job, property purchase, or family event.

Call us on 07 4053 2888 or email contact@parrishfinancial.com.au to enquire about an initial meeting.